What are IB and IGB business lines ?

Value chain approach:

IB/IGB companies achieve most of the impact in their direct value chain that can be influenced by the company. Hence, counting jobs in factory only is not sufficient to capture IB/IGB relevance. Rather the impact in the supply, distribution, consumers and even ownership structure of the firm matters more than pure employment. For example, in an hospital case the impact is on the poor people treated and not the nurses and doctors employed. For an agrobusiness the impact is on the large number of suppliers or consumers (or both) of the product not only the few workers in the processing factory. For a finance company the number of clients matters to calculate impact and not the number of loan officers. Hence a small number of companies can have a large social reach, when the more relevant value chain approach is used. The company size is therefore also not measured by the number of employment but the revenue of the firm.

Innovation:

To work effectively in the markets of the poor and successfully address both business and BoP risks, IB/IGB companies need to be innovative. Business innovations are more relevant for such firms than mere technology innovations. IB/IGB companies are also often innovative in social and environmental areas. Innovative IB/IGB also use their CSR to pilot new business lines.

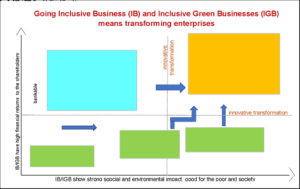

Transformation and triple wins:

By achieving deliberate impact for the poor, the business’ bottom line, and the society, IB/IGB achieve triple-wins and are high relevant for the government. Being innovative and addressing solutions IB/IGB business are also transformative for the economy. They show examples of what the private sector can do to achieve change for the good by doing well. Helping more companies transitioning from a mainstream business (MB), a green business (GB), a grant and NGO based social enterprise (NGO-SE), or from doing traditional corporate social responsibility (CSR) work into an IB/IGB model, initiative or activity is the key purpose of a relevant IB/IGB support program. The chart below shows how IB/IGB companies are transformative in creating impact for more business return and economic growth on the one side, and more and better impact for the poor and the environment on the other and both at the same time. Hence the need for impact-drives-return business coaching and mentoring (IDR-BCM).

For more information on what is IB/IGB see this concept note.

What is the BoP in Ghana ?

Focus on change for the BoP

IB and IGB deliberately create impact for the poor and low-income people. These are the people at the base of the socio-economic pyramid, typically the bottom 40% income groups. However, most IB/IGB do not focus exclusively on the BoP but also the better off income groups. In such cases:

- At least 40% of the impact created should be for the BoP.

- Most IB/IGB companies create 60-80% of their income among the BoP.

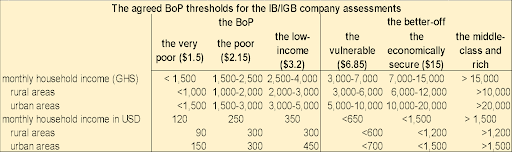

Income Thresholds in Ghana’s IB/IGB Initiative

The income thresholds used in the IB/IGB initiative are derived from national income and expenditure data, aligned with the international poverty discussion, and adjusted to the national conditions.

- While the national minimum income line reflects roughly the international poverty line for poor countries,

- The minimum wage and the country’s poverty line actually reflect the severe poverty line;

- The B40 line is higher and aligned with the more appropriate poverty line for lower middle-income countries like Ghana.

The World Bank’s quasi-relative poverty concept (since 2018) is used to define the BoP in Ghana.

Suggested Income Thresholds for the BoP in Ghana

While thresholds should guide discussions, companies are encouraged to use these flexibly to better reflect their investment and impact cases. The chart below illustrates the income thresholds for very poor, poor, and low-income households that form the BoP.

For more information on the BoP poverty line and how it is calculated, see this concept note.

The Value Chain approach and its implications for the job agenda

Jobs and income opportunities in the value chain:

The public discussion in Ghana has a strong emphasis on job creation. The underlying assumption is that jobs are generated in the formal economy, and these jobs pay well. However, 80% of the jobs in Ghana are in the informal sector, and most of these jobs do not pay well. Encouraging the informal sector to register as formal enterprises does not automatically increase the income opportunities of the people employed in such companies. Rather, employment income is a function of the productivity in a sector, among others, and in Ghana the productivity in industry – and particularly the formal sector, is low.

In emerging economies and developing countries most living standard and income related impact is created in the immediate value chain of a firm, which the company can directly influence. What matters for the IB/IGB discussion is social reach changes of the value chain emphasizing the BoP. For calculating social reach in the IB/IGB discussion only the direct social reach and the direct reach of BoP (not all people) is relevant. For example,

- an agribusiness A may have 60 people in its factory but actually sources all its inputs for that factory directly (contract farming relationships) from 10,000 farmers. Another agrobusiness B may source through 5-20 traders who work with 10,000 farmers. Yet another agrobusiness C is sourcing directly from 10,000 farmers and selling deliberately to 100,000 customers all being better off and agrobusiness D is also sourcing directly from 10,000 farmers and selling directly to 80,000 customers (the rest through traders). The social BoP reach of agrobusiness D is 38,448, that of company A 8.048, that of company B is 48, and that of company C is 6.448. Actually most agrobusinesses are the company B type. In such cases, the IDR-BCM (link to page 4.5). discussion would have a conversation on increasing the total social reach of company B by exploring whether they can engage in direct sourcing.

In another example, a hospital may have 100 employees under its payroll (doctors, nurses, personnel for kitchen, cleaning and administration. Hence the traditional labor market economist would count 100 jobs created as the benefit of the company. However, of these 100 jobs, only estimated 25 are from the BoP communities. And the value addition of a hospital is not the number of doctors and nurses it employs but the number of patients treated. Say the hospital treats 300,000 patients per year. Of these 300,000 people treated, in the case of hospital A only 10% are from BoP communities and in case of hospital B 40%. The total BoP impact (i.e. BoP jobs + BoP value chain beneficiaries) of hospital A would be 30.0125, while in the case of hospital B the number would be 120.025. It is clear that from a public goods perspective, hospital B should be prioritized. The IDR-BCM (link to page 4.5) discussion would emphasize how to increase reach in a hospital business. This is only possible if the services the hospital provides are

- (a) made more affordable (for example cheaper treatment costs and more installment payment or cooperation with health companies),

- (b) the hospital is better accessible for the BoP (for example through geographical location) and

- (c) if the services offered are more relevant for the BoP (for example by adding medicine to the hospital coverage treatment, or by focusing more on specific health needs of the BoP such as basic health services delivery like vaccinations, nutrition related problems etc.).

Why is IB/IGB promotion a multi-stakeholder initiative ?

The IB/IGB initiative for Ghana is designed as a private sector led, government owned, development partners supported and multiple stakeholder implemented program.

The multiple stakeholder implementation is crucial, because many institutions have already programs which would qualify as IB/IGB support programs given their BoP focus. Others have industry support programs that can be targeted to more focus on IB/IGB type of companies. The initiative will include those already existing programs and solicit from the implementation partners commitments on how many companies (or % of financing) the partners will target for IB/IGB companies. These will be documented by the Secretariat (link to page 4.2 in a 3-years rolling action plan. (link to page 4.1), the first perhaps being developed for 2025-2007.

Examples of stakeholders working on IB/IGB is on the partnership page (link to page 5.6).

Measuring impact and transformation

Making the case for special treatments for companies that invest for impact will only be successful in the long run, when the funds placed yield tangible impact on people or planet. Beyond having such impact, this also needs to be transparently and accurately monitored and properly documented. In recent years there is a discussion globally that much of the impact is only claimed and the data used – if any at al – are at a very high and aggregate level, and often not related to the relevant impact shown. There is also raising criticism on general trends to overstate, wrong-report, white-wash and green-wash.

The IB/IGB program has therefore established clear criteria to monitor impact. Ghana companies would only qualify, if they are accredited based on the 48 criteria and 186 benchmarks, all being part of the official IB/IGB accreditation (link to page 4.4) system.

For more information on how the IB/IGB program facilitates better impact monitoring and reporting see page 4.9. (link to page 4.4).

The IB/IGB landscape study

The German Agency for International Cooperation (GIZ) (link to page 5.5) commissioned a landscape study on Inclusive and Green Business in Ghana. The study

- (a) clarifies the IB/IGB concept in the Ghana context,

- (b) identifies and profiles companies with IB/IGB business lines,

- (c) develops strategic recommendations to establish a support program for such firms, and (d) builds ownership and commitment to institutionalize the support program. The study is in cooperation with the Ghana Enterprises Agency (GEA) (link to page 5.6).

It is conducted between November 2023 and January 2025 by a consulting team under CDC Consult (link to this website: https://cdcconsult.com/) (Nana Yaw Amponsah Boadu and Babilo Mahamma, Juanita Djoleto, Lord-Lucas B. Vodzi) and an international expert (Dr. Armin Bauer).

On the company side, 15 companies were identified for the first IB/IGB accreditation. They had in 2023 a consolidated revenue of GhC 988 million and a total social reach of 1.9 million poor and low-income people (2.7 million people in total). By 2030 the companies are projected to grow their revenue to GhC 1.883 million and their social reach to 2.9 million BoP (and 4.5 million in total) people. Imagine how much more can be achieved for the poor and for Ghana, when the IB/IGB initiative is upscaled.

On the policy side the consultant team interviewed 38 organizations from government, business associations, impact investors, business facilitators and development partners, held four stakeholder workshops and various seminars (link to page 5.2), and developed recommendations for a strategic program (link to page 4.1) to create a better enabling environment in support of IB/IGB . The program was discussed in the first Ghana IB/IGB Forum (link to page 5.3),

For institutionalizing IB/IGB support GIZ and the Association of Ghana Enterprises (AGI) (link to page 5.4). concluded a Memorandum of Understanding to do the first IB/IGB accreditation and award, as well as help institutionalizing the program (link to page 4.2) and building further ownership with government and business associations. AGI will also be the proposed chair of the Secretariat for implementing the IB/IGB program from 2025 onwards.

The study will be published in February 2025 and you can download it here (we will establish the link once published).