Transforming Green Businesses (GB) into Inclusive Green Businesses (IGB)

In the public discussion – and following a global trend – here is a strong emphasis on Green Business (GB) in Ghana both among government agencies and development partners but also among companies themselves. However, there is – apart from sector taxonomies, no coherent system to identify such companies through detailed criteria and a transparent identification process. To date, mostly self-claiming is used. The IB/IGB initiative adds to this by offering a transparent company identification tool for Inclusive Green Business.

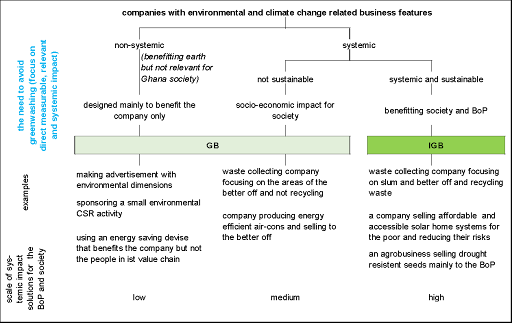

Green Business differ from Inclusive Green Businesses (IGB) in three major areas:

- IGB avoid self-claiming and trickle down assumptions; rather they use identified relevant outcomes to determine their actual results to contribute to a better environment or more climate friendly production.

- The environmental benefits of IGB are assessed not only it their value for the company (e.g. solar panels to reduce the company’s electricity bill), but also in its relevance for the society and economy. And

- IGB need to have direct benefits for the poor and low-income people (BoP) in the environments of the poor.

The IB/IGB discussion has introduced 6 clear criteria to identify Inclusive Green Business. As in the case of IB, the company’s performance is rated against those criteria in low-medium-high results, qualifies through numbers between 0 and 6 (high). The 6 criteria blocks are given below and each block has additional sub-criteria.

- contribution to reduce pollution in the economy

- value addition to manage natural resources

- involvement in reducing the climate footprint (not only of the company, but also more systemically also for the country)

- the quality of its environmental sustainability meaning how comprehensive and deep it addresses environmental and climate challenges in the sector

- how the environmental feature make business sense, and

- how the environmental feature directly benefits the BoP

The scoring of these criteria rating is multiplied with the 6 relevant environmental and 3 relevant climate dimensions an IGB company in the respective sector should address. For the environmental sustainability these are related to challenges and opportunities regarding

- Soil and land preservation,

- Water management,

- Air pollution,

- Biodiversity improvements,

- Waste management, and

- Input reduction and reuse of material (circular economy).

The climate change related dimensions are

- Greenhouse gases mitigation,

- Climate adaptation, and

- Climate resilience practices.

The result is a final scoring for measuring the environmental and climate change impact of an IGB. The maximum impact scoring for IGB (45%) has the same weight than the maximum impact scoring for an IB. Also, to make both company types comparable in their rating, commercial viability (41%), innovation (14%) and strategic intent (100%) weights are the same between IB and IGB.